Why wealthy families must increase their gold exposures... and how to do it smartly with flexgold

For an extended period, familiar factors such as real interest rates, growth forecasts, inflation levels, and the external strength of the US dollar have influenced gold's performance. However, recent developments over the past two years indicate that these conventional elements are no longer adequate to account for the fluctuations in gold prices.

Remarkably, gold has demonstrated a strong ability to withstand increases in real interest rates. This shift signals the rise of new catalysts for gold, which are now complementing traditional bullish influences and providing additional momentum for the precious metal. The evolving landscape surrounding gold emphasises the need to reevaluate its position alongside other asset classes. As a result of various regulatory changes, gold is undergoing a notable revaluation. It is reasonable to expect that the pursuit of alternative investments beyond established financial market players will significantly increase, which could yield positive outcomes for gold.

Between a rock and a hard place: Central Banks vs. Inflation vs. Recession

“Only gold can take the heat of the fire” as an ancient Chinese proverb says.

The assumption that markets regularly fail and that central banks must intervene in a centrally planned manner to avoid recessions misunderstands the true causes.

In reality, recessions are due to the boom and bust cycles inherent in the credit money system, which arise from misallocations caused by artificially low interest rates. These cycles are only exacerbated by central bank interventions and money printing. Interest rate cuts cannot prevent a recession; rather, they are often the original cause, as they promote misallocations during boom phases that later lead to recessions. Central banks can at best mitigate the effects on stock markets by injecting liquidity into the system and countering a collapse of the credit money supply. Given the significant interest rate hikes we have experienced, a recession is inevitable.

The Fed has now cut interest rates for the first time in the past 4 years, even though inflation is not yet fully under control so that the music in the markets doesn't stop playing. If the Fed has to print money again in the next crisis, it will lead to a rapid increase in inflation and market interest rates. As in the 1970s, gold and silver will once again come into focus as inflation-protected investments, attracting investors who will flee to these safe havens due to a lack of alternatives. The markets still believe that the pattern of interest rate cuts and economic recoveries from the past 40 years can continue, unaware that the 1970s could repeat themselves. In this case, last year’s gold rally would merely be a preview of what may lie ahead in the coming years.

1 to 2% is no longer adequate!

According to the latest Campden Wealth European Family Office Report, the average gold share in wealthy portfolios lies around 1 to 2%, while e.g. central banks worldwide have raised their share of gold reserves to an average of 20%!

Do they know more than investors do? Well, we don´t think so.

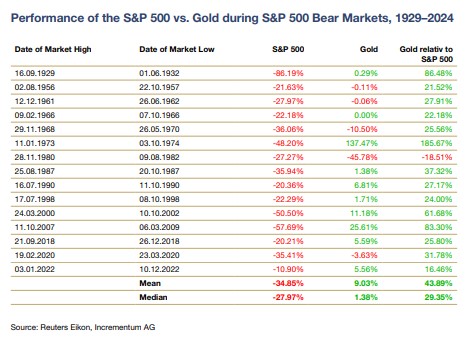

Many studies have been conducted on the effects of different gold shares in classic equity/bond portfolios and on the general impact of changing gold shares on the risk/reward structure of wealthy investment portfolios by Sprott, Incrementum, and others. The conclusions are similar and very clear.

The range of the gold allocation proposed in the studies is between 10% and 19%, depending on the investment period and the other assets held in the portfolio.

Even the lowest allocation in this range is therefore well above the gold exposure of a standard asset allocation.

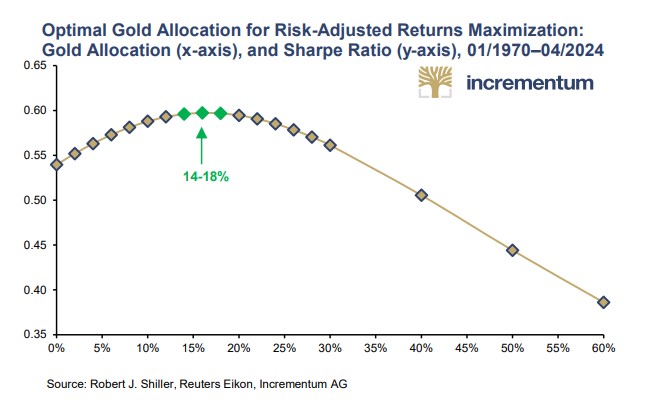

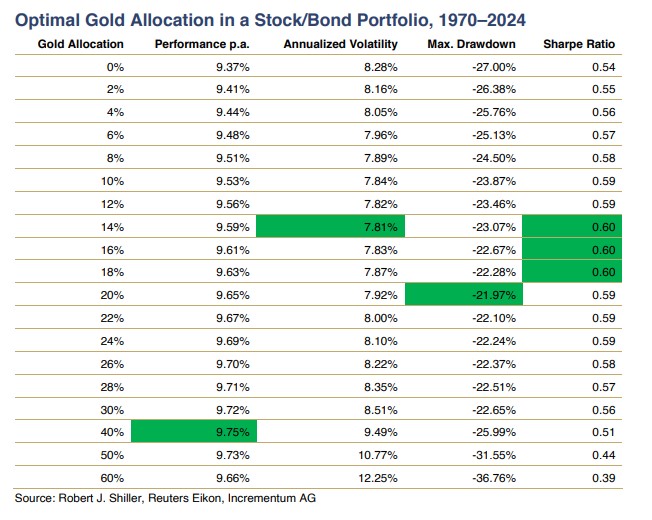

The following chart, which we showed in our presentation at the 21st European Families In Business Forum in Nice, is based on a study period that extends from 1970 to 2024 and includes monthly data on gold as well as the total return indices of the S&P 500 and 10-year US government bonds in US dollars. The calculations show that the integration of gold into an equity/bond portfolio has a clearly positive impact on the Sharpe ratio. The optimum is achieved in an allocation range of 14–18%. An excessive increase in the gold allocation, on the other hand, leads to a decrease in the Sharpe ratio.

Being physically invested without the shortcomings of ETFs or ETCs: flexgold from SOLIT Group AG

With our company SOLIT Group we have been firmly rooted in the precious metals industry for decades. We received a special honour in September 2022 when we were accepted into the circle of Members of the Bullion Market Association (LBMA).

Unlike ETFs or ETCs, our flexgold ecosystem combines the daily tradability of gold at real-time prices (providing complete transparency) with direct physical ownership that is independent of banks. This structure eliminates intermediaries (thus preventing arbitrage) and fully excludes counterparty risks commonly associated with ETCs.

Wealthy families and institutional investors can easily get in touch by sending us an email and asking for our short brochure or a digital meeting.

Alternatively, you can get information here and send us an email referring to this article and what you are interested in.

In the next article, we will expand more on different use cases, notably on how to use gold for Lombard credit liquidity and leverage.

Your Contact Persons for SOLIT's International Advisory and Individual Solutions Services:

Dr. Oliver Wilhelm, Global Head Advisory and Individual Solutions (based in Germany)

Frank Schulze, Global Head Advisory and Individual Solutions (based in Switzerland)